Capital built for dentists.

Single-ticket equipment, de-novo project capital, practice acquisitions. We match you with dental-specialty lenders that underwrite the DDS/DMD income curve — not the same generalist underwriting that declined you.

No hard credit pull to start. Takes about 2 minutes.

Capital for the equipment and the practice.

Equipment, acquisition, de-novo, expansion, working capital, and Section 179 — across the dental specialty lender panel.

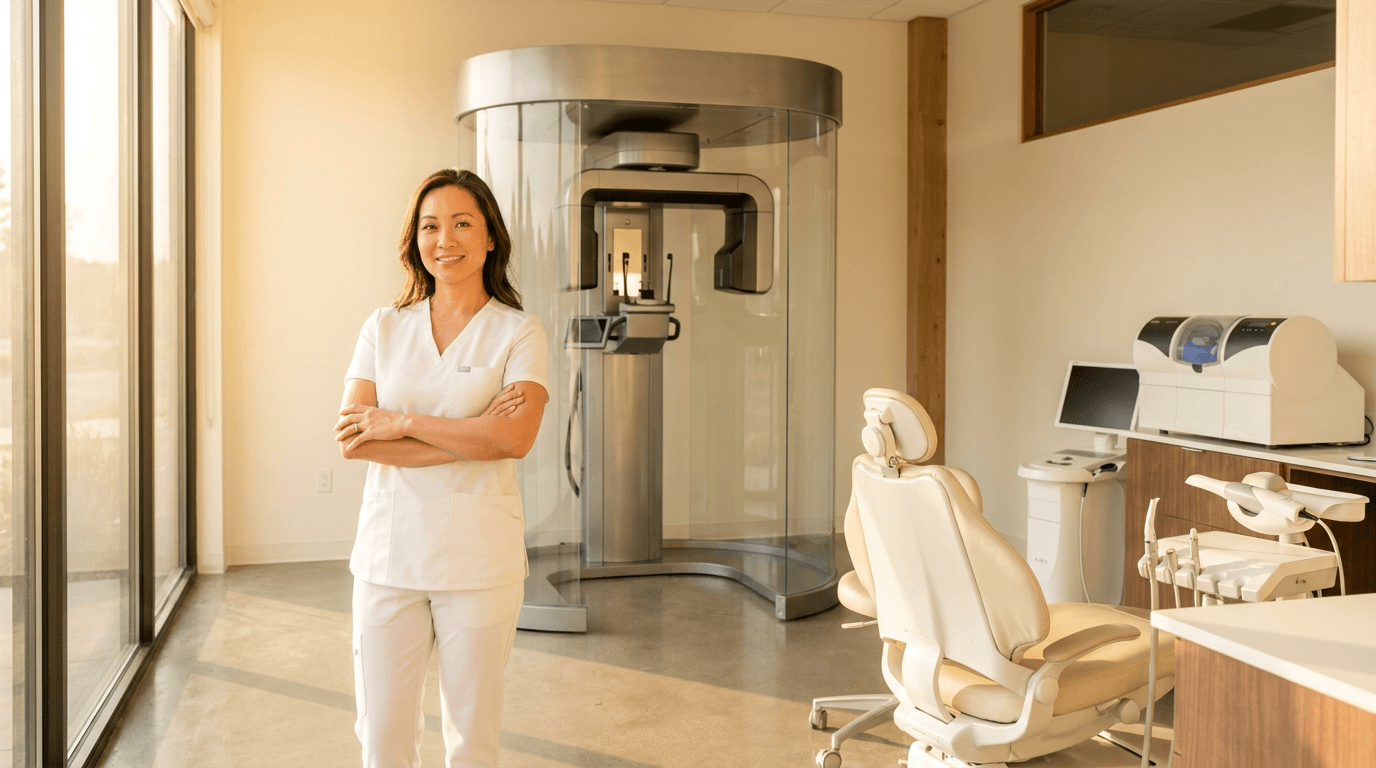

- EquipmentDental equipment financingCBCT, CEREC, scanners, chairs, lasers. 100% common.

- AcquisitionPractice acquisitionUp to 100% on goodwill + equipment + AR.

- De-NovoDe-novo startupBuildout + equipment + working capital, one closing.

- ExpansionExpansion & buildoutAdd operatories, open a second location.

- Working capitalWorking capitalPayroll smoothing, marketing pushes. Cheaper than MCA.

- Section 179Section 179 financingPlace equipment in service by 12/31. Install timelines included.

- $15K–$750KTier A specialty programs

- 5–10 daysTypical time to funded equipment

- Soft-pull firstNo impact on credit

How the money moves.

Five steps, in order. One soft check. One hard pull, and only with the lender you pick. The mechanism is the reason we’re not a broker.

Dental-specialty lenders on our panel.

Built for dental.

Every lender on our panel knows what a CBCT, an EFA, and a de-novo pro-forma are before you start typing.

- Equipment financing — CBCT, CEREC, IOS, chairs, lasers

- Practice acquisition — goodwill + equipment + AR

- De-novo project loans — buildout + equipment + WC

- Section 179 timing built into every term sheet

The lender pays us, not you.

When a matched lender funds your loan, they pay dentalequipment.finance a flat referral fee. It’s disclosed on every term sheet. It does not change your APR.

- No broker points. Zero to you

- Flat fee, disclosed on every term sheet

- Lenders compete on rate and speed, not commission

- One contact. No 7am calls from seven desks

One hard pull.

Only after you pick a lender. Until then it’s a soft match: lenders see your file, you see their offers, and your credit report stays untouched.

- Soft-pull match. No impact on your credit score

- One hard pull, only with the lender you choose

- Equipment in service by 12/31 for Section 179

- E-sign from the operatory; no in-person closings

Banks weren’t built for dentists.

Your production is real. The problem is that most generalist forms don’t understand dental practice economics. Three structural reasons banks say no to working dentists and de-novo owners — none of them about whether you can repay.

Thin business history.

A new owner or a de-novo dentist has 0–2 years of practice financials. Generalist underwriting wants 2+ years of clean P&L and declines what it can't bucket — even when the borrower has $400K of associate production and a 740 FICO.

Single-ticket equipment is outside the box.

A $50K–$150K CBCT or a $90K operatory bundle is a large ask for a generalist platform — outside the median small-business loan, with no comparable in the book. Lenders without dental data route it to manual queue or decline.

Section 179 timing doesn't fit a generalist calendar.

Equipment must be placed in service by 12/31 to claim Section 179 in the current year. Specialty lenders know the install timelines — 4–6 weeks for CBCT, 2–3 weeks for CEREC — and underwrite to the calendar. Generalist banks move on their own schedule, often missing year-end deadlines that materially shift your tax posture.

What a dentalequipment.finance request actually looks like.

Composite illustrative scenarios — not specific borrowers. Each card is built from the kinds of equipment, acquisition, de-novo, and working-capital requests our intake routinely sees.

Owner dentist, 4-op practice

Equipment refresh — CBCT + iTero + chair replacement after 8 years of ownership.

DDS 3 years post-residency

De-novo project: 4-op buildout in a Denver suburb with strong associate production history.

Buyer dentist, acquisition

Acquiring a $1.4M-collections PPO-heavy general practice — 60% multiple, full goodwill + equipment + AR.

Multi-location group, 3 practices

Working capital ahead of a payor renegotiation. PPO writeoff timing creating a 6-week AR gap.

650 typically routes to equipment-leasing programs (EFA / FMV) with APRs in the high teens to low twenties. The structure trades price for access. See /bad-credit-dental-financing.5–10 business days to funded. Equipment financing: 5–10 days for established practices, 10–20 days for new owners or de-novos. Acquisition: 30–60 days end-to-end. De-novo project loans: 30–60 days to approval, then disbursement against milestones.